First Quarter 2023 Housing & Economic Forecast

Overview

We expect the housing market and the overall economy to get worse before they get better. Inflation will continue to slow as the economy slows due to ongoing Fed rate increases. Ultimately, markets crave predictability and until the Fed pauses on rate increases, predictability will be hard to find. Once the Fed pauses, consumers and markets will be able to begin to adjust to a new normal. Until then, market volatility and reduction of access to housing will continue broadly.

Housing prices continue to rise in many markets despite the market slowdown, including Hampton Roads. As the graphic below shows, from REIN MLS, residential sales were down across the board in November, even as inventory rose. Yet, even though sales were down by over 2100 units YoY, inventory rose less than 200 units and prices crept up slightly. This demonstrates that the increase in inventory is miniscule compared to the reduction in buyers and suggests that if we return to a lower rate environment this year, we could again see a critical housing shortage and runaway price increases. The fact that prices are still going up indicates that there is still sufficient demand to drive prices higher despite the slowdown. This is due to the broad and severe housing shortage locally and nationally. There is no indication that this shortage will improve and in fact rising interest rates are cooling the new construction needed to address the shortage. The reduction in home sales as a result of rising rates is not an indication that the shortage is improving, but rather an economic distortion that will likely cause additional upward price pressure once rates stabilize, making homes even more unaffordable and deepening the growing housing crisis.

For buyers, don't expect prices to fall as long as the housing shortage persists. Buyers who are able, should buy now. For sellers, it does not make sense to wait for a higher market before selling. Price growth has slowed to below the rate of inflation. Additionally, continued rate increases and any additional price increases will make it more difficult to find qualified buyers in the future. For both buyers and sellers, we are unlikely to see a better time to buy or sell a house in the next nine to twelve months.

In the Hampton Roads MSA, as in other downturns, we will be less affected due to the necessity of military moves. However, we expect the Year Over Year decline in home sales to persist until rate stability is achieved. Higher rates will mean fewer qualified buyers and buyers qualifying to buy less, but true balance will not return to the market until significant inventory is built. This is a matter of years, not quarters.

The Interest Rate Picture

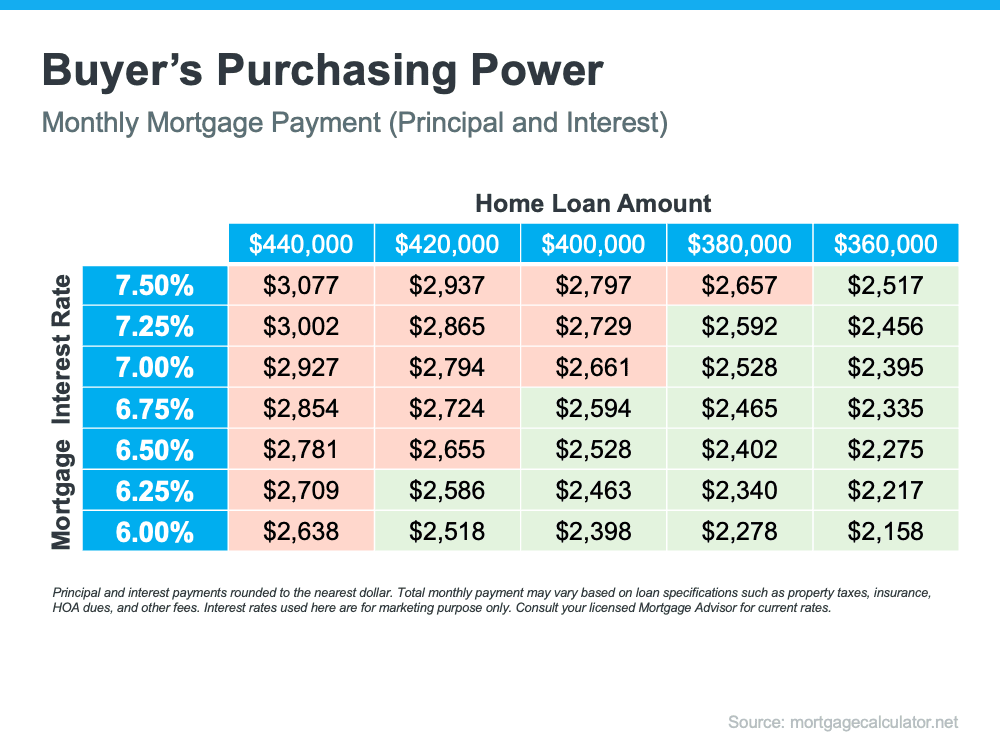

It’s widely expected that the F.O.M.C. will raise the Fed Funds Rate to at least 5.1%. Based on current factors and statements from the Fed, we regard that as a best-case-scenario. We think the most likely scenario is a 0.5% hike at the January/February meeting and at least a .25% hike in March, with a 0.5% increase not off the table at this point. Our opinion is that the final Fed rate will be in the range of 5 – 5.5%. This suggests to us a likely average mortgage rate in the range of 6.9 - 7.5%, once we reach a stable rate environment. We do not know when that will be, but it will probably not be in Q1. Once we reach a more stable market the Fed’s declared intent to keep rates “higher for longer” may become a benefit because consumers will have a better idea of what to expect and have a more reliable idea of how much home they will be able to afford. We believe consumers current buying power is slightly more than it will be when we reach a stable market later in the year. We do think the ultimate stable-environment mortgage rates will settle very close to the 50-year average rate, meaning we will not be in a “new normal” as much as we will be in a historical normal.

Unlike many forecasters, we expect no rate reductions in 2023. The labor market is too strong and wage inflation is too high, in our estimation, to go from high inflation to a recession warranting a change in policy in just the next 12 months. The Fed has been absolutely clear and consistent on their intent to raise rates and keep them up. Throughout the year we have seen many players in the markets behave as if the Fed were not going to do what they said. The Fed has consistently done what they said they were going to do, and we think it is prudent to plan as if that will continue.

We believe we will ultimately have a recession at the end of 2023 or going into 2024, largely as a result of the ongoing Fed policy. The recession may begin sooner, but the effects seem unlikely to be severe enough this year to cause rate reductions. However, markets are very volatile at this time and constant reassessment is required.

Buyer Expectations

Buyers who are able to buy, should not wait. Buyers should not expect prices to fall as long as the housing shortage persists, unless there is a severe recession. A recession this severe is highly unlikely. The housing reductions we are seeing in most of the nation and especially in Hampton Roads are primarily properties that were priced above market value and are often properties purchased as flips or other investments. They are not being sold at reduced market prices but being adjusted to market rates, in most cases. The idea of a real estate bubble or widespread price reductions in this market environment are myths in our opinion.

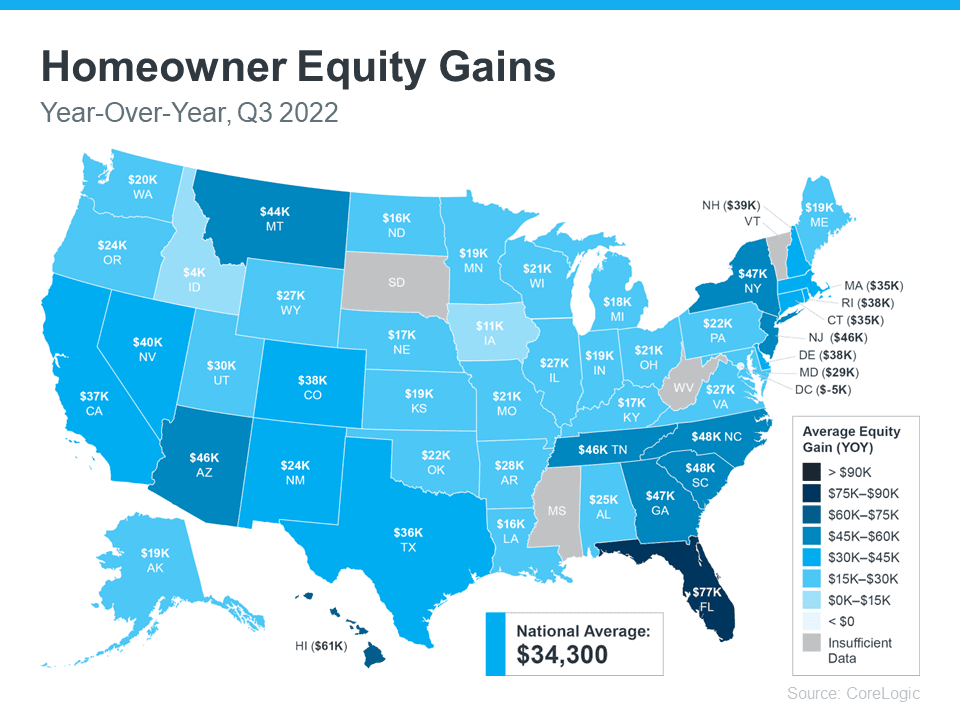

In the case of private homeowners, there is still high demand for their homes due to the shortage, and they will be reluctant to sell at prices lower than in the previous year, as it would represent a loss of equity and wealth to them. Many will not move unless they must and many who do have to move will rent out their homes, rather than take a loss. The rise in home equity has dramatically increased wealth across the country, and while some markets may be inflated, Virginia has been on the lower end of those increases and deep reductions are even more unlikely here than in markets that saw more dramatic growth.

By most estimates, buyers currently have 20-30% less buying power than they did a year ago. Since home price reductions are generally from over-inflated and institutional prices, we do not think these reductions will bring significant relief to new buyers. Rather, buyers’ expectations of what they can afford will have to adjust and that will take time. This situation will also put additional upward price pressure on the limited number of entry-level homes. We believe the buyers who adjust their expectations and act quickly will be able to obtain homes at the best prices available for many months or years to come. Those who delay, run the risk of being priced out of the market as inventory levels drop again this spring season and they may face additional rate increases.

Seller Expectations

Sellers can expect continued demand for their properties and for prices to hold steady or increase slightly. However, home prices are rising slower than inflation currently, so to delay in selling, in hopes of a higher sales price, may mean a worse net position. We expect this to be the case for at least Q1 and probably beyond.

With rate reductions unlikely and household savings beginning to decline, expect buyers to be able to buy less house. Entry level homes should continue to sell quickly. The more expensive homes are, the longer it will take, and the more that will be required to sell them in terms of marketing and concessions. This condition should endure throughout the year and is not an indication of a balanced market. This is the previously mentioned market distortion caused by Fed policy that is slowing demand without increasing supply. Therefore, this still is, and will remain, a pronounced sellers’ market for the foreseeable future. The challenge for sellers is to be found first by qualified buyers and to secure them. Sellers with quality inventory and the ability to reach qualified buyers will still enjoy faster than historical rates of sales and price stability or slight increases.

This forecast contains forward looking statements, the accuracy of which cannot be guaranteed, and no investment or financial decision should be based on these statements alone. Please consult your financial or realty professionals before making any financial or realty decision. This forecast is the intellectual property of The Home Run Team Ltd. and any sharing, re-posting, or quoting of it must be properly attributed to The Home Run Team.

There's a myth about down payments that hold a lot of buyers back; here's what to know to not get fooled.

Let’s take a look at some historical data to show what’s happened in the housing market during each recession, going all the way back to the 1980s.

Right now, it's a tale of two markets, and knowing which one you’re in makes a huge difference when you move.

Just because the economies down doesn't mean home prices will follow; in fact, it may be the opposite.

If you put the latest data into context, it’s clear there’s no reason to think this is a repeat of the last housing crash.

Here’s the thing: the market’s shifting. And it might be time to hit play again.

If you put your home search on hold because you couldn't find anything you liked in your budget, it's time to try again.

Savvy sellers are jumping off the fence and back into the market. And here’s why.

Here’s what most buyers don’t always think about: the longer you wait, the more buying could cost you.

We're here to help people live wealthier lives and enjoy more freedom by educating and guiding them through their lifelong real estate journey. Whether you're buying a home, looking to sell or relocate, or are an investor, we can help you. No agents will work harder for you, because to us, going to bat for you, isn't work. That's just what you do when you're a team.